The COUNTREG Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecification of RegressorsMissing ValuesPoisson RegressionConway-Maxwell-Poisson RegressionNegative Binomial RegressionZero-Inflated Count Regression OverviewZero-Inflated Poisson RegressionZero-Inflated Conway-Maxwell-Poisson RegressionZero-Inflated Negative Binomial RegressionVariable SelectionPanel Data AnalysisComputational ResourcesNonlinear Optimization OptionsCovariance Matrix TypesDisplayed OutputOUTPUT OUT= Data SetOUTEST= Data SetODS Table NamesODS Graphics

-

Examples

- References

The count regression model for panel data can be derived from the Poisson regression model. Consider the multiplicative one-way panel data model,

where

Here, ![]() are the individual effects.

are the individual effects.

In the fixed-effects model, the ![]() are unknown parameters. The fixed-effects model can be estimated by eliminating

are unknown parameters. The fixed-effects model can be estimated by eliminating ![]() by conditioning on

by conditioning on ![]() .

.

In the random-effects model, the ![]() are independent and identically distributed (iid) random variables, in contrast to the fixed effects model. The random-effects

model can then be estimated by assuming a distribution for

are independent and identically distributed (iid) random variables, in contrast to the fixed effects model. The random-effects

model can then be estimated by assuming a distribution for ![]() .

.

In the Poisson fixed-effects model, conditional on ![]() and parameter

and parameter ![]() ,

, ![]() is iid Poisson-distributed with parameter

is iid Poisson-distributed with parameter ![]() , and

, and ![]() does not include an intercept. Then, the conditional joint density for the outcomes within the

does not include an intercept. Then, the conditional joint density for the outcomes within the ![]() th panel is

th panel is

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\sum _{t=1}^{T_{i}}y_{it}] & = & P[y_{i1},\ldots ,y_{iT_{i}},\sum _{t=1}^{T_{i}}y_{it}] / P[\sum _{t=1}^{T_{i}}y_{it}] \\ & = & P[y_{i1},\ldots ,y_{iT_{i}}]/P[\sum _{t=1}^{T_{i}}y_{it}] \end{eqnarray*}](images/etsug_countreg0257.png)

Because ![]() is iid Poisson(

is iid Poisson(![]() ),

), ![]() is the product of

is the product of ![]() Poisson densities. Also,

Poisson densities. Also, ![]() is Poisson(

is Poisson(![]() ). Then,

). Then,

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\sum _{t=1}^{T_{i}}y_{it}] & = & \frac{\sum _{t=1}^{T_{i}} (\exp (-\mu _{it}) \mu _{it}^{y_{it}} / y_{it}! )}{\exp (-\sum _{t=1}^{T_{i}} \mu _{it}) \left( \sum _{t=1}^{T_{i}} \mu _{it} \right)^{\sum _{t=1}^{T_{i}} y_{it} } / \left( \sum _{t=1}^{T_{i}} y_{it} \right)!} \\ & = & \frac{\exp (-\sum _{t=1}^{T_{i}} \mu _{it}) \left( \prod _{t=1}^{T_{i}} \mu _{it}^{y_{it}} \right) \left( \prod _{t=1}^{T_{i}} y_{it}! \right) }{\exp ( -\sum _{t=1}^{T_{i}} \mu _{it}) \prod _{t=1}^{T_{i}} \left( \sum _{s=1}^{T_{i}} \mu _{is} \right)^{y_{it}} / \left( \sum _{t=1}^{T_{i}} y_{it} \right)!} \\ & = & \frac{(\sum _{t=1}^{T_{i}} y_{it})!}{(\prod _{t=1}^{T_{i}} y_{it}!)} \prod _{t=1}^{T_{i}} \left(\frac{\mu _{it}}{\sum _{s=1}^{T_{i}} \mu _{is}}\right)^{y_{it}} \\ & = & \frac{(\sum _{t=1}^{T_{i}} y_{it})!}{(\prod _{t=1}^{T_{i}} y_{it}!)} \prod _{t=1}^{T_{i}} \left(\frac{\lambda _{it}}{\sum _{s=1}^{T_{i}} \lambda _{is}}\right)^{y_{it}} \\ \end{eqnarray*}](images/etsug_countreg0263.png)

Thus, the conditional log-likelihood function of the fixed-effects Poisson model is given by

The gradient is

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial \bbeta } & = & \sum _{i=1}^{N} \sum _{t=1}^{T_{i}} y_{it}x_{it} - \sum _{i=1}^{N} \sum _{t=1}^{T_{i}} \left[ \frac{y_{it} \sum _{s=1}^{T_{i}} \left( \exp (\mathbf{x}_{is}\bbeta ) \mathbf{x}_{is} \right)}{\sum _{s=1}^{T_{i}} \exp (\mathbf{x}_{is}\bbeta )} \right] \\ & = & \sum _{i=1}^{N} \sum _{t=1}^{T_{i}} y_{it} (\mathbf{x}_{it}-\mathbf{\bar{x}}_{i}) \end{eqnarray*}](images/etsug_countreg0265.png)

where

In the Poisson random-effects model, conditional on ![]() and parameter

and parameter ![]() ,

, ![]() is iid Poisson-distributed with parameter

is iid Poisson-distributed with parameter ![]() , and the individual effects,

, and the individual effects, ![]() , are assumed to be iid random variables. The joint density for observations in all time periods for the

, are assumed to be iid random variables. The joint density for observations in all time periods for the ![]() th individual,

th individual, ![]() , can be obtained after the density

, can be obtained after the density ![]() of

of ![]() is specified.

is specified.

Let

so that ![]() and

and ![]() :

:

Let ![]() . Because

. Because ![]() is conditional on

is conditional on ![]() and parameter

and parameter ![]() is iid Poisson(

is iid Poisson(![]() ), the conditional joint probability for observations in all time periods for the

), the conditional joint probability for observations in all time periods for the ![]() th individual,

th individual, ![]() , is the product of

, is the product of ![]() Poisson densities:

Poisson densities:

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\lambda _{i},\alpha _{i}] & = & \prod _{t=1}^{T_{i}} P[y_{it}| \lambda _{i}, \alpha _{i}]\\ & = & \prod _{t=1}^{T_{i}}\left[ \frac{\exp (-\mu _{it}) \mu _{it}^{y_{it}}}{y_{it}!} \right] \\ & = & \left[ \prod _{t=1}^{T_{i}} \frac{e^{-\alpha _{i}\lambda _{it}}(\alpha _{i}\lambda _{it})^{y_{it}}}{y_{it}!} \right] \\ & = & \left[ \prod _{t=1}^{T_{i}} \lambda _{it}^{y_{it}}/y_{it}! \right] \left( e^{-\alpha _{i} \sum _{t} \lambda _{it}} \alpha _{i}^{\sum _{t} y_{it}} \right) \end{eqnarray*}](images/etsug_countreg0277.png)

Then, the joint density for the ![]() th panel conditional on just the

th panel conditional on just the ![]() can be obtained by integrating out

can be obtained by integrating out ![]() :

:

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\lambda _{i}] & = & \int _{0}^{\infty } P[y_{i1},\ldots ,y_{iT}|\lambda _{i},\alpha _{i}] g(\alpha _{i}) d\alpha _{i} \\ & = & \frac{\theta ^{\theta }}{\Gamma (\theta )} \left[ \prod _{t=1}^{T_{i}} \frac{\lambda _{it}^{y_{it}}}{y_{it}!} \right] \int _{0}^{\infty } \exp (-\alpha _{i} \sum _{t} \lambda _{it}) \alpha _{i}^{\sum _{t} y_{it}} \alpha _{i}^{\theta -1} \exp (-\theta \alpha _{i}) d\alpha _{i} \\ & = & \frac{\theta ^{\theta }}{\Gamma (\theta )} \left[ \prod _{t=1}^{T_{i}} \frac{\lambda _{it}^{y_{it}}}{y_{it}!} \right] \int _{0}^{\infty } \exp \left[ -\alpha _{i} \left( \theta + \sum _{t} \lambda _{it} \right) \right] \alpha _{i}^{\theta + \sum _{t} y_{it}-1} d\alpha _{i} \\ & = & \left[ \prod _{t=1}^{T_{i}} \frac{\lambda _{it}^{y_{it}}}{y_{it}!} \right] \frac{\Gamma (\theta + \sum _{t} y_{it})}{\Gamma (\theta )} \\ & & \times \left(\frac{\theta }{\theta +\sum _{t} \lambda _{it}} \right)^{\theta } \left(\theta + \sum _{t} \lambda _{it} \right)^{-\sum _{t} y_{it}} \\ & = & \left[ \prod _{t=1}^{T_{i}} \frac{\lambda _{it}^{y_{it}}}{y_{it}!} \right] \frac{\Gamma (\alpha ^{-1}+ \sum _{t} y_{it})}{\Gamma (\alpha ^{-1})} \\ & & \times \left(\frac{\alpha ^{-1}}{\alpha ^{-1}+\sum _{t} \lambda _{it}} \right)^{\alpha ^{-1}} \left(\alpha ^{-1} + \sum _{t} \lambda _{it} \right)^{-\sum _{t} y_{it}} \end{eqnarray*}](images/etsug_countreg0278.png)

where ![]() is the overdispersion parameter. This is the density of the Poisson random-effects model with gamma-distributed random effects.

For this distribution,

is the overdispersion parameter. This is the density of the Poisson random-effects model with gamma-distributed random effects.

For this distribution, ![]() and

and ![]() ; that is, there is overdispersion.

; that is, there is overdispersion.

Then the log-likelihood function is written as

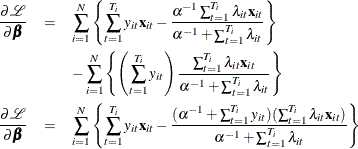

![\begin{eqnarray*} \mathcal{L} & = & \sum _{i=1}^{N} \left\{ \sum _{t=1}^{T_{i}} \ln (\frac{\lambda _{it}^{y_{it}}}{y_{it}!}) + \alpha ^{-1} \ln (\alpha ^{-1}) -\alpha ^{-1} \ln (\alpha ^{-1}+\sum _{t=1}^{T_{i}}\lambda _{it}) \right\} \\ & & + \sum _{i=1}^{N} \left\{ - \left( \sum _{t=1}^{T_{i}}y_{it} \right) \ln \left(\alpha ^{-1}+\sum _{t=1}^{T_{i}}\lambda _{it}\right) \right. \\ & & \left. \hspace*{0.3in} + \ln \left[\Gamma \left(\alpha ^{-1}+ \sum _{t=1}^{T_{i}}y_{it} \right)\right] -\ln (\Gamma (\alpha ^{-1})) \right\} \end{eqnarray*}](images/etsug_countreg0282.png)

The gradient is

and

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial \alpha } & = & \sum _{i=1}^{N} \left\{ -\alpha ^{-2} \left[ [1+ \ln (\alpha ^{-1})] - \frac{(\alpha ^{-1}+\sum _{t=1}^{T_{i}} y_{it})}{(\alpha ^{-1})+ \sum _{t=1}^{T_{i}}\lambda _{it}} - \ln \left(\alpha ^{-1} + \sum _{t=1}^{T_{i}} \lambda _{it} \right) \right] \right\} \\ & + & \sum _{i=1}^{N} \left\{ -\alpha ^{-2} \left[ \frac{\Gamma (\alpha ^{-1}+ \sum _{t=1}^{T_{i}} y_{it})}{\Gamma (\alpha ^{-1} +\sum _{t=1}^{T_{i}} y_{it})} -\frac{\Gamma (\alpha ^{-1})}{\Gamma (\alpha ^{-1})} \right] \right\} \end{eqnarray*}](images/etsug_countreg0284.png)

where ![]() ,

, ![]() and

and ![]() is the digamma function.

is the digamma function.

This section shows the derivation of a negative binomial model with fixed effects. Keep the assumptions of the Poisson-distributed dependent variable

But now let the Poisson parameter be random with gamma distribution and parameters ![]() ,

,

where one of the parameters is the exponentially affine function of independent variables ![]() . Use integration by parts to obtain the distribution of

. Use integration by parts to obtain the distribution of ![]() ,

,

![\begin{eqnarray*} P\left[y_{it}\right]& = & \int _{0}^{\infty }\frac{e^{-\mu _{it}}\mu _{it}^{y_{it}}}{y_{it}!}f\left(\mu _{it}\right)d\mu _{it}\\ & = & \frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}\right)\Gamma \left(y_{it}+1\right)}\left(\frac{\delta }{1+\delta }\right)^{\lambda _{it}}\left(\frac{1}{1+\delta }\right)^{y_{it}} \end{eqnarray*}](images/etsug_countreg0292.png)

which is a negative binomial distribution with parameters ![]() . Conditional joint distribution is given as

. Conditional joint distribution is given as

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\sum _{t=1}^{T_{i}}y_{it}]& =& \left(\prod _{t=1}^{T_{i}}\frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}\right)\Gamma \left(y_{it}+1\right)}\right)\\ & & \times \left(\frac{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)\Gamma \left(\sum _{t=1}^{T_{i}}y_{it}+1\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right) \end{eqnarray*}](images/etsug_countreg0293.png)

Hence, the conditional fixed-effects negative binomial log-likelihood is

![\begin{eqnarray*} \mathcal{L}& = & \sum _{i=1}^{N}\left[\log \Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)+\log \Gamma \left(\sum _{t=1}^{T_{i}}y_{it}+1\right)-\log \Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)\right]\\ & & +\sum _{i=1}^{N}\sum _{t=1}^{T_{i}}\left[\log \Gamma \left(\lambda _{it}+y_{it}\right)-\log \Gamma \left(\lambda _{it}\right)-\log \Gamma \left(y_{it}+1\right)\right] \end{eqnarray*}](images/etsug_countreg0294.png)

The gradient is

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial \beta }& = & \sum _{i=1}^{N}\left[\left(\frac{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)}-\frac{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right)\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}\right]\\ & & +\sum _{i=1}^{N}\frac{\Gamma \left(\sum _{t=1}^{T_{i}}y_{it}+1\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}y_{it}+1\right)}\\ & & +\sum _{i=1}^{N}\sum _{t=1}^{T_{i}}\left[\left(\frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}+y_{it}\right)}-\frac{\Gamma \left(\lambda _{it}\right)}{\Gamma \left(\lambda _{it}\right)}\right)\lambda _{it}\mathbf{x}_{it}-\frac{\Gamma \left(y_{it}+1\right)}{\Gamma \left(y_{it}+1\right)}\right] \end{eqnarray*}](images/etsug_countreg0295.png)

This section describes the derivation of negative binomial model with random effects. Suppose

with the Poisson parameter distributed as gamma,

where its parameters are also random:

Assume that the distribution of a function of ![]() is beta with parameters

is beta with parameters ![]() :

:

Explicitly, the beta density with ![]() domain is

domain is

where ![]() is the beta function. Then, conditional joint distribution of dependent variables is

is the beta function. Then, conditional joint distribution of dependent variables is

Integrating out the variable ![]() yields the following conditional distribution function:

yields the following conditional distribution function:

![\begin{eqnarray*} P[y_{i1},\ldots ,y_{iT_{i}}|\mathbf{x}_{i1},\ldots ,\mathbf{x}_{iT_{i}}]& = & \int _{0}^{1}\left[\prod _{t=1}^{T_{i}}\frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}\right)\Gamma \left(y_{it}+1\right)}z_{i}^{\lambda _{it}}\left(1-z_{i}\right)^{y_{it}}\right]f\left(z_{i}\right)dz_{i}\\ & = & \frac{\Gamma \left(a+b\right)\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a\right)\Gamma \left(b\right)\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\\ & & \times \prod _{t=1}^{T_{i}}\frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}\right)\Gamma \left(y_{it}+1\right)} \end{eqnarray*}](images/etsug_countreg0305.png)

Consequently, the conditional log-likelihood function for a negative binomial model with random effects is

![\begin{eqnarray*} \mathcal{L}& = & \sum _{i=1}^{N}\left[\log \Gamma \left(a+b\right)+\log \Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)+\log \Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)\right]\\ & & -\sum _{i=1}^{N}\left[\log \Gamma \left(a\right)+\log \Gamma \left(b\right)+\log \Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)\right]\\ & & +\sum _{i=1}^{N}\sum _{t=1}^{T_{i}}\left[\log \Gamma \left(\lambda _{it}+y_{it}\right)-\log \Gamma \left(\lambda _{it}\right)-\log \Gamma \left(y_{it}+1\right)\right] \end{eqnarray*}](images/etsug_countreg0306.png)

The gradient is

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial \beta }& = & \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}+\frac{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}\right]\\ & & -\sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}\right]\\ & & +\sum _{i=1}^{N}\sum _{t=1}^{T_{i}}\left[\left(\frac{\Gamma \left(\lambda _{it}+y_{it}\right)}{\Gamma \left(\lambda _{it}+y_{it}\right)}-\frac{\Gamma \left(\lambda _{it}\right)}{\Gamma \left(\lambda _{it}\right)}\right)\lambda _{it}\mathbf{x}_{it}-\frac{\Gamma \left(y_{it}+1\right)}{\Gamma \left(y_{it}+1\right)}\right] \end{eqnarray*}](images/etsug_countreg0307.png)

and

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial a}& = & \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b\right)}{\Gamma \left(a+b\right)}+\frac{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}\right]\\ & & -\sum _{i=1}^{N}\left[\frac{\Gamma \left(a\right)}{\Gamma \left(a\right)}+\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right] \end{eqnarray*}](images/etsug_countreg0308.png)

and

![\begin{eqnarray*} \frac{\partial \mathcal{L}}{\partial b}& = & \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b\right)}{\Gamma \left(a+b\right)}+\frac{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}\right]\\ & & -\sum _{i=1}^{N}\left[\frac{\Gamma \left(b\right)}{\Gamma \left(b\right)}+\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right] \end{eqnarray*}](images/etsug_countreg0309.png)