The PANEL Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecifying the Input DataSpecifying the Regression ModelUnbalanced DataMissing ValuesComputational ResourcesRestricted EstimatesNotationOne-Way Fixed-Effects ModelTwo-Way Fixed-Effects ModelBalanced PanelsUnbalanced PanelsBetween EstimatorsPooled EstimatorOne-Way Random-Effects ModelTwo-Way Random-Effects ModelParks Method (Autoregressive Model)Da Silva Method (Variance-Component Moving Average Model)Dynamic Panel EstimatorLinear Hypothesis TestingHeteroscedasticity-Corrected Covariance MatricesHeteroscedasticity- and Autocorrelation-Consistent Covariance MatricesR-SquareSpecification TestsPanel Data Poolability TestPanel Data Unit Root TestsTroubleshootingCreating ODS GraphicsOUTPUT OUT= Data SetOUTEST= Data SetOUTTRANS= Data SetPrinted OutputODS Table Names

-

Example

- References

The Da Silva method assumes that the observed value of the dependent variable at the tth time point on the ith cross-sectional unit can be expressed as

where

-

is a vector of explanatory variables for the tth time point and ith cross-sectional unit

is a vector of explanatory variables for the tth time point and ith cross-sectional unit

-

is the vector of parameters

is the vector of parameters

-

is a time-invariant, cross-sectional unit effect

is a time-invariant, cross-sectional unit effect

-

is a cross-sectionally invariant time effect

is a cross-sectionally invariant time effect

-

is a residual effect unaccounted for by the explanatory variables and the specific time and cross-sectional unit effects

is a residual effect unaccounted for by the explanatory variables and the specific time and cross-sectional unit effects

Since the observations are arranged first by cross sections, then by time periods within cross sections, these equations can be written in matrix notation as

where

Here 1 ![]() is an

is an ![]() vector with all elements equal to 1, and

vector with all elements equal to 1, and ![]() denotes the Kronecker product.

denotes the Kronecker product.

The following conditions are assumed:

-

is a sequence of nonstochastic, known

is a sequence of nonstochastic, known  vectors in

vectors in  whose elements are uniformly bounded in . The matrix X has a full column rank p.

whose elements are uniformly bounded in . The matrix X has a full column rank p.

-

is a

is a  constant vector of unknown parameters.

constant vector of unknown parameters.

-

a is a vector of uncorrelated random variables such that

and

and  ,

,  .

.

-

b is a vector of uncorrelated random variables such that

and

and  where

where  and

and  .

.

-

is a sample of a realization of a finite moving-average time series of order

is a sample of a realization of a finite moving-average time series of order  for each i ; hence,

for each i ; hence,

![\[ e_{it}={\alpha }_{0} {\epsilon }_{it}+ {\alpha }_{1} {\epsilon }_{it-1}+{\ldots }+ {\alpha }_{m} {\epsilon }_{it-m} \; \; \; \; t=1,{\ldots },\mi {T} ; i=1,{\ldots },\mi {N} \]](images/etsug_panel0361.png)

where

are unknown constants such that

are unknown constants such that  and

and  , and

, and  is a white noise process for each

is a white noise process for each  —that is, a sequence of uncorrelated random variables with

—that is, a sequence of uncorrelated random variables with  , and

, and  . for

. for  are mutually uncorrelated.

are mutually uncorrelated.

-

The sets of random variables

,

,  , and

, and  for are mutually uncorrelated.

for are mutually uncorrelated.

-

The random terms have normal distributions

and

and  for

for  and

and  .

.

If assumptions 1–6 are satisfied, then

and

where ![]() is a

is a ![]() matrix with elements

matrix with elements ![]() as follows:

as follows:

where ![]() for

for ![]() . For the definition of

. For the definition of ![]() ,

, ![]() ,

, ![]() , and

, and ![]() , see the section Fuller and Battese’s Method.

, see the section Fuller and Battese’s Method.

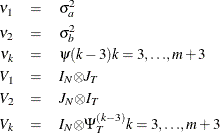

The covariance matrix, denoted by V, can be written in the form

where ![]() , and, for k =1,

, and, for k =1,![]() , m,

, m, ![]() is a band matrix whose kth off-diagonal elements are 1’s and all other elements are 0’s.

is a band matrix whose kth off-diagonal elements are 1’s and all other elements are 0’s.

Thus, the covariance matrix of the vector of observations y has the form

where

The estimator of ![]() is a two-step GLS-type estimator—that is, GLS with the unknown covariance matrix replaced by a suitable estimator of V. It is obtained by substituting Seely estimates for the scalar multiples

is a two-step GLS-type estimator—that is, GLS with the unknown covariance matrix replaced by a suitable estimator of V. It is obtained by substituting Seely estimates for the scalar multiples ![]() .

.

Seely (1969) presents a general theory of unbiased estimation when the choice of estimators is restricted to finite dimensional vector

spaces, with a special emphasis on quadratic estimation of functions of the form ![]() .

.

The parameters ![]() (i =1,

(i =1,![]() , n) are associated with a linear model E(y )=X

, n) are associated with a linear model E(y )=X ![]() with covariance matrix

with covariance matrix ![]() where

where ![]() (i =1,

(i =1, ![]() , n) are real symmetric matrices. The method is also discussed by Seely (1970b, 1970a); Seely and Zyskind (1971). Seely and Soong (1971) consider the MINQUE principle, using an approach along the lines of Seely (1969).

, n) are real symmetric matrices. The method is also discussed by Seely (1970b, 1970a); Seely and Zyskind (1971). Seely and Soong (1971) consider the MINQUE principle, using an approach along the lines of Seely (1969).