The SURVEYLOGISTIC Procedure

- Overview

- Getting Started

-

Syntax

PROC SURVEYLOGISTIC StatementBY StatementCLASS StatementCLUSTER StatementCONTRAST StatementDOMAIN StatementEFFECT StatementESTIMATE StatementFREQ StatementLSMEANS StatementLSMESTIMATE StatementMODEL StatementOUTPUT StatementREPWEIGHTS StatementSLICE StatementSTORE StatementSTRATA StatementTEST StatementUNITS StatementWEIGHT Statement

PROC SURVEYLOGISTIC StatementBY StatementCLASS StatementCLUSTER StatementCONTRAST StatementDOMAIN StatementEFFECT StatementESTIMATE StatementFREQ StatementLSMEANS StatementLSMESTIMATE StatementMODEL StatementOUTPUT StatementREPWEIGHTS StatementSLICE StatementSTORE StatementSTRATA StatementTEST StatementUNITS StatementWEIGHT Statement -

DetailsMissing ValuesModel SpecificationModel FittingSurvey Design InformationLogistic Regression Models and ParametersVariance EstimationDomain AnalysisHypothesis Testing and EstimationLinear Predictor, Predicted Probability, and Confidence LimitsOutput Data SetsDisplayed OutputODS Table NamesODS Graphics

-

Examples

- References

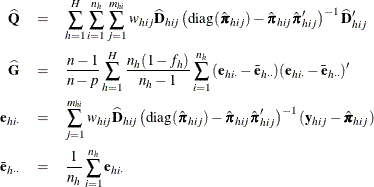

The Taylor series (linearization) method is the most commonly used method to estimate the covariance matrix of the regression coefficients for complex survey data. It is the default variance estimation method used by PROC SURVEYLOGISTIC.

Using the notation described in the section Notation, the estimated covariance matrix of model parameters ![]() by the Taylor series method is

by the Taylor series method is

where

and ![]() is the matrix of partial derivatives of the link function

is the matrix of partial derivatives of the link function ![]() with respect to

with respect to ![]() and

and ![]() and the response probabilities

and the response probabilities ![]() are evaluated at

are evaluated at ![]() .

.

If you specify the TECHNIQUE=NEWTON option in the MODEL statement to request the Newton-Raphson algorithm, the matrix ![]() is replaced by the negative (expected) Hessian matrix when the estimated covariance matrix

is replaced by the negative (expected) Hessian matrix when the estimated covariance matrix ![]() is computed.

is computed.