The VARMAX Procedure

- Overview

-

Getting Started

-

Syntax

-

DetailsMissing ValuesVARMAX ModelDynamic Simultaneous Equations ModelingImpulse Response FunctionForecastingTentative Order SelectionVAR and VARX ModelingBayesian VAR and VARX ModelingVARMA and VARMAX ModelingModel Diagnostic ChecksCointegrationVector Error Correction ModelingI(2) ModelMultivariate GARCH ModelingOutput Data SetsOUT= Data SetOUTEST= Data SetOUTHT= Data SetOUTSTAT= Data SetPrinted OutputODS Table NamesODS GraphicsComputational Issues

-

Examples

- References

The ![]() th-order VAR process is written as

th-order VAR process is written as

with ![]() .

.

Equivalently, it can be written as

with ![]() .

.

For stationarity, the VAR process must be expressible in the convergent causal infinite MA form as

where ![]() with

with ![]() , where

, where ![]() denotes a norm for the matrix

denotes a norm for the matrix ![]() such as

such as ![]() . The matrix

. The matrix ![]() can be recursively obtained from the relation

can be recursively obtained from the relation ![]() ; it is

; it is

where ![]() and

and ![]() for

for ![]() .

.

The stationarity condition is satisfied if all roots of ![]() are outside of the unit circle. The stationarity condition is equivalent to the condition in the corresponding VAR(1) representation,

are outside of the unit circle. The stationarity condition is equivalent to the condition in the corresponding VAR(1) representation,

![]() , that all eigenvalues of the

, that all eigenvalues of the ![]() companion matrix

companion matrix ![]() be less than one in absolute value, where

be less than one in absolute value, where ![]() ,

, ![]() , and

, and

![\begin{eqnarray*} \Phi = \left[ \begin{matrix} \Phi _1 & \Phi _2 & \cdots & \Phi _{p-1} & \Phi _{p} \\ I_ k & 0 & \cdots & 0 & 0 \\ 0 & I_ k & \cdots & 0 & 0 \\ \vdots & \vdots & \ddots & \vdots & \vdots \\ 0 & 0 & \cdots & I_ k & 0 \\ \end{matrix} \right] \end{eqnarray*}](images/etsug_varmax0513.png)

If the stationarity condition is not satisfied, a nonstationary model (a differenced model or an error correction model) might be more appropriate.

The following statements estimate a VAR(1) model and use the ROOTS option to compute the characteristic polynomial roots:

proc varmax data=simul1; model y1 y2 / p=1 noint print=(roots); run;

Figure 35.44 shows the output associated with the ROOTS option, which indicates that the series is stationary since the modulus of the eigenvalue is less than one.

Figure 35.44: Stationarity (ROOTS Option)

| Roots of AR Characteristic Polynomial | |||||

|---|---|---|---|---|---|

| Index | Real | Imaginary | Modulus | Radian | Degree |

| 1 | 0.77238 | 0.35899 | 0.8517 | 0.4351 | 24.9284 |

| 2 | 0.77238 | -0.35899 | 0.8517 | -0.4351 | -24.9284 |

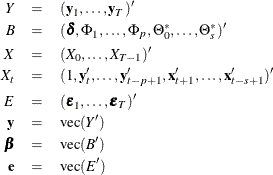

Consider the stationary VAR(![]() ) model

) model

where ![]() are assumed to be available (for convenience of notation). This can be represented by the general form of the multivariate

linear model,

are assumed to be available (for convenience of notation). This can be represented by the general form of the multivariate

linear model,

where

with vec denoting the column stacking operator.

The conditional least squares estimator of ![]() is

is

and the estimate of ![]() is

is

where ![]() is the residual vectors. Consistency and asymptotic normality of the LS estimator are that

is the residual vectors. Consistency and asymptotic normality of the LS estimator are that

where ![]() converges in probability to

converges in probability to ![]() and

and ![]() denotes convergence in distribution.

denotes convergence in distribution.

The (conditional) maximum likelihood estimator in the VAR(![]() ) model is equal to the (conditional) least squares estimator on the assumption of normality of the error vectors.

) model is equal to the (conditional) least squares estimator on the assumption of normality of the error vectors.

As before, vec denotes the column stacking operator and vech is the corresponding operator that stacks the elements on and below the diagonal. For any ![]() matrix

matrix ![]() , the commutation matrix

, the commutation matrix ![]() is defined as

is defined as ![]() ; the duplication matrix

; the duplication matrix ![]() is defined as

is defined as ![]() ; the elimination matrix

; the elimination matrix ![]() is defined as

is defined as ![]() .

.

The asymptotic distribution of the impulse response function (Lütkepohl, 1993) is

where ![]() and

and

where ![]() is a

is a ![]() matrix and

matrix and ![]() is a

is a ![]() companion matrix.

companion matrix.

The asymptotic distribution of the accumulated impulse response function is

where ![]() .

.

The asymptotic distribution of the orthogonalized impulse response function is

where ![]() ,

, ![]() ,

, ![]() ,

,

and ![]() with

with ![]() and

and ![]() .

.

Let ![]() be arranged and partitioned in subgroups

be arranged and partitioned in subgroups ![]() and

and ![]() with dimensions

with dimensions ![]() and

and ![]() , respectively (

, respectively (![]() ); that is,

); that is, ![]() with the corresponding white noise process

with the corresponding white noise process ![]() . Consider the VAR(

. Consider the VAR(![]() ) model with partitioned coefficients

) model with partitioned coefficients ![]() for

for ![]() as follows:

as follows:

The variables ![]() are said to cause

are said to cause ![]() , but

, but ![]() do not cause

do not cause ![]() if

if ![]() . The implication of this model structure is that future values of the process

. The implication of this model structure is that future values of the process ![]() are influenced only by its own past and not by the past of

are influenced only by its own past and not by the past of ![]() , where future values of

, where future values of ![]() are influenced by the past of both

are influenced by the past of both ![]() and

and ![]() . If the future

. If the future ![]() are not influenced by the past values of

are not influenced by the past values of ![]() , then it can be better to model

, then it can be better to model ![]() separately from

separately from ![]() .

.

Consider testing ![]() , where

, where ![]() is a

is a ![]() matrix of rank

matrix of rank ![]() and

and ![]() is an

is an ![]() -dimensional vector where

-dimensional vector where ![]() . Assuming that

. Assuming that

you get the Wald statistic

For the Granger causality test, the matrix ![]() consists of zeros or ones and

consists of zeros or ones and ![]() is the zero vector. See Lütkepohl (1993) for more details of the Granger causality test.

is the zero vector. See Lütkepohl (1993) for more details of the Granger causality test.

The vector autoregressive model with exogenous variables is called the VARX(![]() ,

,![]() ) model. The form of the VARX(

) model. The form of the VARX(![]() ,

,![]() ) model can be written as

) model can be written as

The parameter estimates can be obtained by representing the general form of the multivariate linear model,

where

The conditional least squares estimator of ![]() can be obtained by using the same method in a VAR(

can be obtained by using the same method in a VAR(![]() ) modeling. If the multivariate linear model has different independent variables that correspond to dependent variables, the

SUR (seemingly unrelated regression) method is used to improve the regression estimates.

) modeling. If the multivariate linear model has different independent variables that correspond to dependent variables, the

SUR (seemingly unrelated regression) method is used to improve the regression estimates.

The following example fits the ordinary regression model:

proc varmax data=one;

model y1-y3 = x1-x5;

run;

This is equivalent to the REG procedure in the SAS/STAT software:

proc reg data=one;

model y1 = x1-x5;

model y2 = x1-x5;

model y3 = x1-x5;

run;

The following example fits the second-order lagged regression model:

proc varmax data=two;

model y1 y2 = x / xlag=2;

run;

This is equivalent to the REG procedure in the SAS/STAT software:

data three;

set two;

xlag1 = lag1(x);

xlag2 = lag2(x);

run;

proc reg data=three;

model y1 = x xlag1 xlag2;

model y2 = x xlag1 xlag2;

run;

The following example fits the ordinary regression model with different regressors:

proc varmax data=one;

model y1 = x1-x3, y2 = x2 x3;

run;

This is equivalent to the following SYSLIN procedure statements:

proc syslin data=one vardef=df sur;

endogenous y1 y2;

model y1 = x1-x3;

model y2 = x2 x3;

run;

From the output in Figure 35.20 in the section Getting Started: VARMAX Procedure, you can see that the parameters, XL0_1_2, XL0_2_1, XL0_3_1, and XL0_3_2 associated with the exogenous variables, are not significant. The following example fits the VARX(1,0) model with different regressors:

proc varmax data=grunfeld; model y1 = x1, y2 = x2, y3 / p=1 print=(estimates); run;

Figure 35.45: Parameter Estimates for the VARX(1, 0) Model

| XLag | |||

|---|---|---|---|

| Lag | Variable | x1 | x2 |

| 0 | y1 | 1.83231 | _ |

| y2 | _ | 2.42110 | |

| y3 | _ | _ | |

As you can see in Figure 35.45, the symbol ‘_’ in the elements of matrix corresponds to endogenous variables that do not take the denoted exogenous variables.